What is a First Time Home Buyer Loan?

A First Time Home Buyer is considered someone who has not had ownership interest in a home for the past 3 years. So if you never owned a home before, or if you had a home and sold it for whatever reason over 3 years ago, you would qualify for this type of loan. There are several Types of Loan Programs and providers that help FTHB’s get into a home loan which can be more affordable that a traditional loan. Not all Banks, Credit Unions, Mortgage Bankers or Mortgage Programs offer all of the programs that we do.

What programs are offered?

- FHA - Government backed program

- VA – Federally backed program

- USDA – Government backed program

- WHEDA - Bond Program/State backed programs

- Non QM – Non-traditional Programs backed by wholesale lenders

- Home Ready - Fannie Mae (Federal National Mortgage Association)

- Home Possible - Freddie Mac (Federal Home Loan Corporation)

What Properties are Eligible for First Time Home Buyers/Affordable Lending Programs?

All programs are a good fit for Single Family residences, Condominiums (except USDA), Manufactured homes (not conventional), Town homes, and Foreclosed or Short Sale properties. For multi-unit properties most offer 1-2 Unit (except VA & USDA). For 3-4 Unit, you would need to go with an FHA or Conventional Program.

Experience is the most critical aspect when choosing the right professional to work with. With over 30 years of experience, I keep up with ever changing guidelines and help you select the correct program for your personal situation. I do this by taking the time offer program comparisons so you can make the best decision for you and your family. Furthermore, my team of highly trained operation professionals make the process seamless and stress free. When you work with Epic, you get the whole team effort to keep everything moving along according to plan. Communication is the key and we pride ourselves on top-notch communications along the way. I have dozens of handpicked investors and lenders so I can shop for you to obtain the best possible program with a fantastic rate that fits your needs. The educational process continues with suggested and at times required Homebuyer Education. I walk with you step by step throughout the process. Once my clients are approved, I help them with the buying process along with their Real Estate Agent or can recommend a great one to work with.

Advantages of a First Time Home Buyer Loan:

A first-time homebuyer loan, also known as a first-time homebuyer program or mortgage, offers several advantages to individuals purchasing a home for the first time. Some of the key advantages include:

- Lower Down Payment: First-time homebuyer loans often have lower down payment requirements compared to conventional mortgages. They typically allow borrowers to put down a smaller percentage of the home's purchase price, making it more accessible for individuals who may have limited savings.

- Easier Qualification: First-time homebuyer loans may have more lenient qualification criteria compared to conventional mortgages. Lenders often consider factors such as credit score, debt-to-income ratio, and employment history, taking into account that first-time homebuyers may have less established credit or limited work history.

- Reduced Interest Rates: Some first-time homebuyer loan programs offer lower interest rates or special incentives for eligible borrowers. This can result in significant savings over the life of the loan, making homeownership more affordable.

- Assistance with Closing Costs: Many first-time homebuyer programs provide assistance with closing costs, which can be a significant expense when purchasing a home. These programs may offer grants or loans to cover a portion of the closing costs, reducing the financial burden on the buyer.

- Education and Counseling: First-time homebuyer loan programs often require or provide access to educational resources and counseling services. These resources aim to educate buyers about the homebuying process, financial responsibilities, and long-term homeownership, empowering them to make informed decisions.

- Flexible Credit Requirements: Some first-time homebuyer loan programs are more flexible with credit requirements. They may consider alternative credit history, such as rental payments or utility bills, making it easier for individuals with limited or nontraditional credit histories to qualify for a mortgage.

- Availability of Government-backed Loans: First-time homebuyer loans often include government-backed loan options, such as those offered by the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA). These loans typically have more flexible guidelines and lower down payment requirements, making homeownership more accessible to first-time buyers.

It's important to note that the advantages and specific terms of first-time homebuyer loans can vary depending on the program, lender, and location. It's recommended to research and compare different loan options to find the one that best suits your needs and financial situation.

FHA Loans

- 96.5% Financing (3.5% down payment)

- Upfront Mortgage Insurance Premium normally financed

- Monthly Mortgage Insurance (PMI) not determined by Fico (Conventional)

- FICO Scores down to 580

- Interest Rates can be less than Conventional loans

- No Pre-payment Penalty

- Low Closing Costs

- Less Than Perfect Credit Is Welcome

VA Loans

- 100% Financing ($0 down payment)

- No Monthly Mortgage Insurance (PMI)

- FICO Scores down to 580

- Lower Interest Rates than Conventional loans

- No Pre-payment Penalty

- Low Closing Costs

- Less Than Perfect Credit Is Welcome

- Loans Up To $2,000,000

USDA Loans

- 100% Financing ($0 down payment)

- Must be in a federally designated Rural Area

- No Monthly Mortgage Insurance (PMI)

- FICO Scores down to 580

- Lower Interest Rates than Conventional loans

- No Pre-payment Penalty

- Low Closing Costs

- Less Than Perfect Credit Is Welcome

WHEDA Loans

- 97% Financing (3% down payment)

- 3% Second Mortgage allowed (making the down payment $0)

- Discounted Monthly Mortgage Insurance (PMI)

- Income Restricted to 80% County Medium Income for lower PMI

- 100% County Medium Income use traditional PMI

- Household Income Used to Qualify

- FICO Scores down to 620

- Lower Interest Rates than Conventional loans

- No Pre-payment Penalty

- Purchase Price Limits exist

- Homebuyer Education Required

Non-QM Affordable Loan

- 97% Financing (3% down payment)

- Discounted Monthly Mortgage Insurance (PMI)

- Income Restricted to 100% Area Medium Income (use look-up tool on-line)

- Qualifying income used (only the borrower on the loan)

- FICO Scores down to 620

- No Pre-payment Penalty

- Homebuyer Education Required

Conventional Loans

- Home Ready (Fannie Mae) & Home Possible (Freddie Mac)

- 97% Financing (3% down payment)

- Discounted Monthly Mortgage Insurance (PMI)

- Income Restricted to 80% Area Medium Income (use look-up tool on-line)

- Qualifying income used (benefit: can use only the borrower on the loan)

- FICO Scores down to 620

- Lower Interest Rates than Conventional loans

- No Pre-payment Penalty

- Homebuyer Education Required

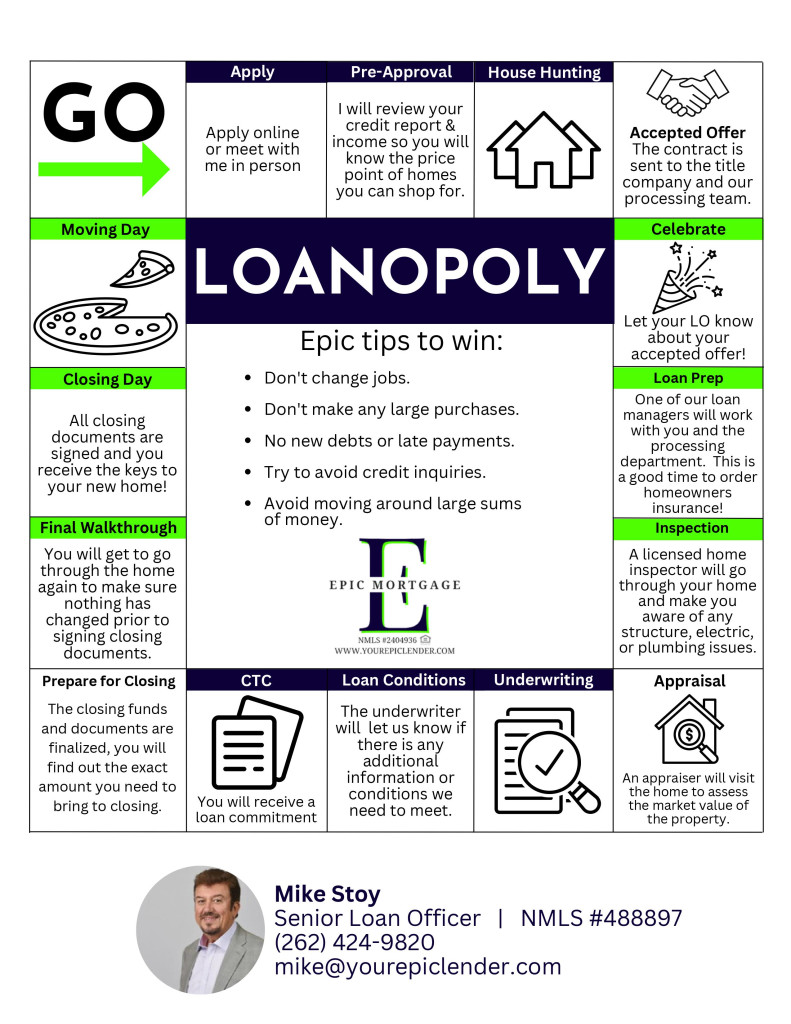

Loan Approval Process Explained

Set an appointment with a Mortgage Advisor who is an expert in consultation. You will be given a checklist of documentation to start the process.

A general list would include:

- 2 years most recent W2’s or 1099’s

- 30 days most recent paycheck stubs

- 2 most recent bank statements and your driver’s license

- If you are an independent contractor, 100% commissions, or self-employed you will need to supply the last two years federal tax returns.

- With some programs it is good to strengthen the file with other assets statements like investments, stocks and retirement accounts.

- If you are going for a VA loan you will need to provide a certificate of eligibility from the VA, DD214 or statement of service.

- Once those items are provided and reviewed and we run your credit report and submit your loan into the automated underwriting system for approval.

- We then provide you and your agent with a preapproval letter within 24 hours.

- Once pre-approved, you should contact your Real Estate Agent and provide your specifications of the home of your dreams.

- Once you received an accepted offer to purchase, you or your agents will send all of the contractual documentation to us.

- We will send you a Loan Estimate estimating and summarizing your loan numbers minus any credits you will receive at closing.

- We will then submit your loan to underwriting. You will receive a Conditional Approval within a couple of days.

- A conditional approval can require things like Title Appraisal, Homeowners Insurance, and proof of earnest money.

- Once all of those conditions are met, your loan will go back into underwriting for Final Approval. Upon receipt of Final Approval and no later than 3 days prior to closing your will get a Preliminary Closing Disclosure.

- Once we get the final Settlement Statement from the Seller-side, we will provide you with a Final Closing Disclosure.

- Closing will be scheduled normally at a Title Company.

- As soon as the VA loan conditions have been gathered and the underwriter signs them off, then approx. 24-48 later the final loan documents will be drawn up and will need to be signed in the presence of a notary.

- At that point, you will then be instructed to wire the funds needed to close on your purchase to title/escrow and will officially close on your purchase within a day or two later.

What else should I know about VA Loans?

If you should have any questions about VA Loans or about this process and would like to schedule an appointment, please click here or call me at 619-208-6499. I am here to help you at either my Chula Vista office or my San Diego Office.

What is a Certificate of Eligibility?

Every veteran has to meet one of the following service requirements before they can obtain VA loans:

- 181 days of service during peacetime

- 90 days of service during war time

- 6 years of service in the Reserves or National Guard

- Some surviving spouses of veterans killed in the line of duty are also eligible.

Mortgage lenders are required to provide proof of a veteran’s service before starting the VA loan process. The COE serves as that proof and tells a lender that an applicant has officially met the minimum service requirement.

How do I get my Certificate of Eligibility?

Three ways:

- Ask your lender. The easiest and best method of obtaining a Certificate of Eligibility. We can help you with this process if you do not have one.

- Apply online.

- Apply via mail.

Thanks for serving our country, I look forward to serving you!